MCA Stacking: How to Escape the Debt Spiral

Multiple merchant cash advances pulling from the same account daily is one of the fastest ways to collapse a business. Here's how the spiral works and how to get out.

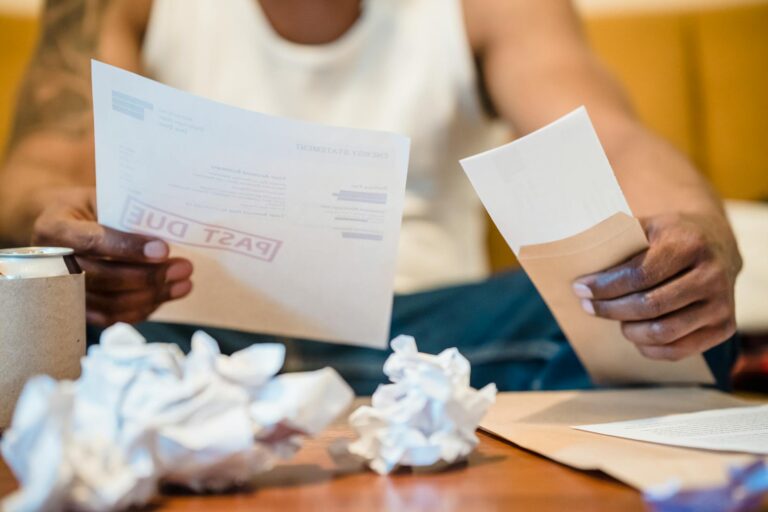

When One Advance Becomes Five

It starts reasonably enough. Your business hits a slow month, a big client pays late, or equipment breaks down at the worst possible time. You take a merchant cash advance to bridge the gap. It works. You pay it back — mostly. Then you need another one while the first is still running. Then a third to keep payroll covered while the second is debiting daily. Before long, you have four or five funders pulling from your account simultaneously, and you can’t remember the last time your bank balance had room to breathe.

This is MCA stacking, and it is one of the most destructive financial patterns a small business can land in — not because owners are irresponsible, but because MCA companies approve advances based on gross revenue, not on how many other advances are already draining that same revenue. Each new funder looks at your deposits and sees a fundable business. None of them see the full picture.

The good news: stacking is not a dead end. We’ve seen businesses with five, six, even seven simultaneous funders negotiate their way out through structured settlement and resolution strategies — without taking another advance to do it. Results vary and are not guaranteed, but the path out is real, and it starts with understanding how the spiral actually works.

The Daily Debit Math That Breaks Businesses

The numbers aren’t complicated, but they are brutal when you lay them out side by side. A single $50,000 MCA at a 1.40 factor rate means $70,000 back. Over a 90-business-day term, that’s approximately $778 leaving your account every single morning — before payroll, before suppliers, before rent.

Stack a second advance on top of that at similar terms and you’re at $1,556 a day. A third brings the daily total to $2,334. For a business doing $600,000 in annual revenue, that’s roughly $840,000 in annualized debit payments — 140% of gross revenue. The math cannot hold.

According to the Federal Reserve’s 2024 Report on Employer Firms, small businesses with fewer financing options increasingly turn to high-cost alternative financing — but the report also shows that businesses with high debt burdens are far more likely to report financial distress. The daily debit structure is designed to capture revenue first. By the time operational expenses need to be paid, what’s left may not be enough.

Why Funders Keep Approving Stacked Deals

There is no centralized database of outstanding MCA obligations. When a funder evaluates your business for a new advance, they pull your bank statements and processing history. They see revenue coming in. What they don’t see — or don’t check — is how many other advances are already debiting against that same revenue stream every morning.

MCA companies file UCC-1 blanket liens against business assets when they fund an advance. These filings are public record. But not every funder pulls UCC reports before approving a deal, and even when they do, a UCC-1 doesn’t prevent another funder from filing one right behind it. Multiple funders can hold competing security interests in the same receivables simultaneously — all debiting the same account.

The FTC’s 2022 enforcement action against RCG Advances spotlighted how aggressive MCA underwriting — approving deals for businesses already in financial distress — can accelerate collapse rather than provide real relief. Understanding this dynamic matters because it means the stack is not entirely your fault. It’s a structural problem built into how MCA underwriting works.

Five Signs You're Already Deep in the Stack

Most business owners don’t use the word “stacking” to describe their situation — they just know something is very wrong. Here are the clearest warning signs:

- You took a new advance to cover payments on an existing one. This is the defining moment. Once you’re borrowing to repay borrowing, the stack is compounding faster than revenue can keep up.

- Multiple funders are calling about bounced or late debits. Managing lender calls is consuming time you should be spending running your business.

- Your daily account balance is consistently near zero. Revenue arrives and disappears into debits the same day. There is no buffer for a slow week.

- You’ve received a default notice or acceleration letter. This means a funder is demanding the full remaining balance immediately — not just the daily debit amount.

- Your debt service is consuming more than 15% of gross revenue. Lenders — traditional or alternative — generally consider 10–15% of gross revenue to be the ceiling for sustainable debt service. Past that threshold, the business is running on borrowed time.

If two or more of these describe your situation right now, the window for the best resolution options is open — but it won’t stay open indefinitely. The earlier the intervention, the more options are on the table.

The Options That Actually Move the Needle

Calling each funder individually and asking for a payment reduction rarely solves a multi-funder stack. Each funder negotiates only for themselves, and none of them are motivated to reduce their payments so another funder can get paid faster. You need a coordinated strategy, not a series of individual phone calls.

The options that produce real results:

- Hardship or modification request: Works best before default, with documented evidence of financial distress. Some funders will extend the term or reduce the daily debit temporarily.

- ACH revocation: You have the legal right to revoke a funder’s ACH authorization through your bank. This stops the daily debit immediately — but it triggers default on the MCA contracts. This step should never be taken without a plan for what comes next.

- Negotiated settlement: After default, many funders will settle for a discounted lump sum rather than pursue expensive litigation. We’ve seen original balances reduced by 50%, 70%, even more through structured negotiation. This is the option that has produced the most dramatic results for stacked business owners. Results vary and are not guaranteed.

- Subchapter V Chapter 11: For businesses with qualifying debt under approximately $3.1 million, Subchapter V bankruptcy offers a streamlined reorganization path with legal protection across all creditors simultaneously. It requires a business attorney and a formal court filing.

The right option depends on where you are in the default timeline, how many funders are involved, and whether litigation has started. Creditors may not always agree to proposed terms — but options exist at every stage.

Real Settlement Numbers from Past Stacking Cases

Here is what structured negotiation has actually produced in past cases — not projections, not estimates, but completed settlements:

- A six-figure balance of $96,675 resolved for $20,210 — a 79% reduction

- A $50,000 purchased amount settled at $15,000 — 70% reduction

- A $211,591 judgment avoided entirely and settled for $61,000 — 72% reduction

- A $28,613 balance reduced to $2,861 — 90% reduction

These results came from businesses that had already defaulted — which is important context. Funders know that a lawsuit is expensive. They know that a business in default may have limited assets to recover. A negotiated settlement at $0.25 on the dollar, paid today, is often more attractive to them than a court process that costs them legal fees and months of staff time.

Past performance does not predict future results, and results vary significantly based on the funder, the contract terms, the timing, and the specific financial situation. Not every case achieves these outcomes — but these numbers represent what’s been possible when experienced specialists handle the negotiation on behalf of the business owner.

What to Do Right Now: Start Here

Start with a full accounting of the stack: every funder, every outstanding balance, every daily debit amount, and every contract status (current, delinquent, or in default). Most business owners are surprised by the total when it’s laid out clearly. That number is the foundation of any real strategy.

Then talk to an MCA Relief Specialist before taking any action on your own — especially before you call funders, revoke ACH authorizations, or stop payments. The order of operations matters. Steps taken in the wrong sequence can close off options that would otherwise have been available.

This article is general information about commercial business debt — it is not consumer debt advice, and it is not legal or financial guidance for your specific situation. Every restructuring case is different. But one conversation with a specialist who has handled cases like yours can change the picture completely. The path through stacked MCA debt exists. You don’t have to find it alone.

Photo credits: Featured image by Nicola Barts on Pexels; Section 1 by Kampus Production on Pexels; Section 2 by RDNE Stock project on Pexels; Section 3 by cottonbro studio on Pexels; Section 4 by RDNE Stock project on Pexels; Section 5 by Kampus Production on Pexels; Section 6 by Ron Lach on Pexels; Section 7 by Kampus Production on Pexels.